Beauty’s New Battleground: Shelf Space vs. Scroll Space

How TikTok and Amazon Are Redefining Discovery, Loyalty, and Purchase and What It Means for the Next Era of Beauty Retail

Over the past decade, beauty retail has evolved from department store counters to the polished walls of Sephora and Ulta. But today, we’re at another inflection point — one that is reshaping how consumers discover, shop, and remain loyal to beauty brands.

Jefferies’ latest deep dive into the beauty retail landscape confirms what many of us in early-stage investing have felt intuitively: the platforms driving discovery are now the ones driving purchase and TikTok Shop and Amazon are emerging as the biggest winners.

Here’s what we’re seeing and what it means for our portfolio and the broader beauty founder community.

1. From Counters to Clicks: The Evolution of Beauty Retail

Just 15 years ago, prestige beauty was synonymous with the department store. Heritage brands like Clinique, Estée Lauder, Lancome and Dior built their distribution strategies around Saks, Nordstrom, and Bloomingdale’s elegant, separated brand counters that supported mono-brand consumption.

Then came Ulta and Sephora, providing consumers with new access and an experience that changed shopping habits and behaviors. These specialty retailers pioneered a “self-service” multi-brand beauty retail format that empowered consumers to freely mix, match, and explore without the high pressure sales counter.

Ulta blended mass-market and high-end products under one roof, something department stores never did (they focused only on prestige).

Sephora curated trendier and niche brands, offering exclusives that department stores didn’t carry.

Overall, this multi-brand specialty model dethroned the mono-brand department store retail model, reflecting a broader consumer shift away from loyalty to any one label and toward a deep, discerning loyalty to individual products.

Today’s beauty consumer is highly educated and product-obsessed. They are loyal to the serum that delivers results, the mascara that doesn’t flake, or the lipstick with the perfect finish rather than to a single brand across categories. This behavioral shift both fueled and was reinforced by the open-sell, discovery-driven environment pioneered by Sephora, where shoppers could freely compare, test, and curate their own routines across brands. In many ways, the space encouraged exploration, which then accelerated the decline of traditional brand monogamy. Consumers became less brand loyal because the environment empowered them to be product loyal, rewarding efficacy, experience, and innovation over heritage or brand prestige.

Now, the evolution continues: and today’s beauty floor is digital.

It lives on TikTok. It lives on Amazon. And increasingly, it lives in the creator economy.

As a result, we are seeing specialty retail growth stall with the growing structural shift of beauty consumption to online channels. Sephora and Ulta, whose rise contributed so significantly to the demise of department stores, are now losing share to Amazon and TikTok Shop as consumers continue to build trust in purchasing beauty products there.

TBV POV: Legacy brands that once resisted Amazon for fear of brand dilution now have dedicated storefronts and are leveraging Prime’s promise of convenience and trust. In parallel, TikTok is creating a discovery-to-checkout pipeline that bypasses traditional retail entirely.

2. Amazon’s Beauty Moment — Once Avoided, Now Embraced

For years, prestige beauty brands refused to sell on Amazon. The platform was seen as too transactional, too price-driven, and too risky for counterfeits, a clear threat to luxury positioning.

As investors, we also had our concerns. We used to believe that Amazon was a great place for monetizing brand awareness, but not a great place for building it.

But the tides have turned.

Today, Amazon offers curated brand store pages, exclusive distribution agreements, and premium fulfillment that rivals traditional retailers. Consumers, now more than ever, trust the platform and Amazon’s premium beauty segment has become a major growth driver.

A major driver of this shift is Amazon’s evolution into a primary search engine for product discovery. As TikTok virality fuels consumer demand, Amazon is often the first destination where that momentum converts into sales. The connection is so strong, it’s no surprise that #TikTokMadeMeBuyIt has become a cultural and commercial phenomenon.1

Founder insight: Don’t discount Amazon in your long-term channel mix. For replenishable categories like skincare, haircare and ingestibles, it’s become a crucial part of the prestige funnel, particularly for consumers who prioritize convenience and consistency. Even small brands with little brand awareness can capitalize on the significant growth of this “convenient to purchase” channel.

3. Sephora’s Defensive Strategy: Exclusivity and Control

As competition heats up, Sephora is doubling down on exclusivity. With platforms like Amazon and TikTok Shop gaining traction, Sephora is pushing back by requiring certain brands to limit distribution elsewhere in order to reap the benefits of exclusive brand status.

This effort isn’t just about revenue. It’s about preserving Sephora’s role as the curator of prestige and trend. The brand’s partnership with Kohl’s has expanded reach, but behind the scenes, Sephora is working hard to retain its gatekeeper status by prioritizing unique, high-growth brands (think Rare Beauty, Glossier, and Makeup by Mario) and discouraging Amazon or potentially even TikTok cross-sell.

For early-stage brands, Sephora exclusivity can be a powerful lever — a growth accelerant that should not be underestimated. From brand visibility and merchandising to margins and financial support, we always encourage brands to leverage exclusivity and weigh trade-offs very carefully. N.B.: Non-exclusive brands with broader distribution and slowing trends are more at risk of being pulled from shelves.

TBV guidance: For brands in (or aiming for) Sephora, channel strategy must be surgical. Consider launch timing, exclusivity windows, and what your long-term omnichannel roadmap looks like before you sign the dotted line.

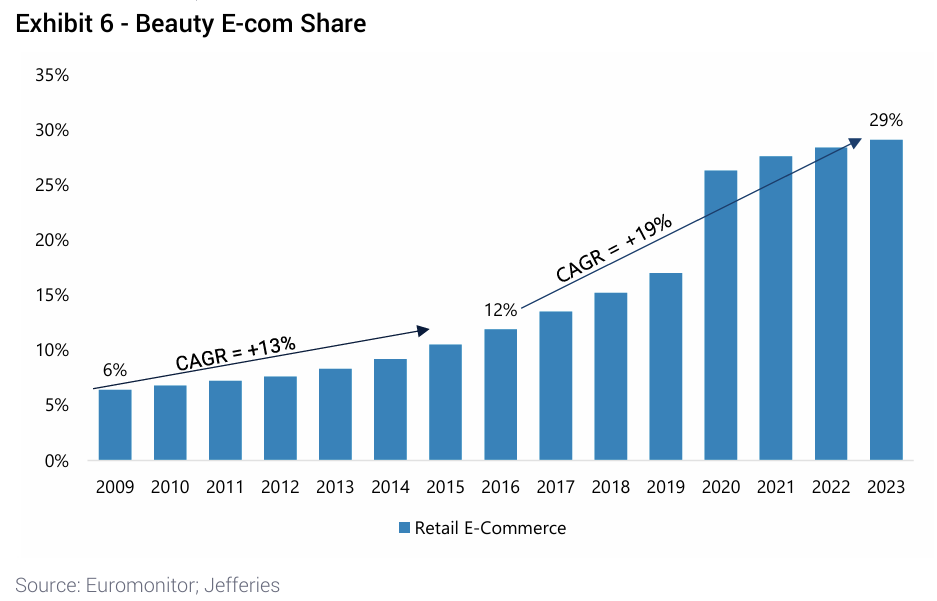

4. E-Commerce Is the Default — Especially for Emerging Consumers

Ecommerce is expected to grow from 29% to 40–45% of beauty sales by 2028, led by TikTok Shop and Amazon.2

Unlike traditional retailers, these platforms combine discovery, trust, and conversion in one scroll. TikTok Shop already converts 44% of US users, while Amazon leverages Prime shipping and reputation to lead the category in skincare, haircare, and even color cosmetics.3

What this means for founders:

If your brand isn’t visible on TikTok & Amazon, you’re leaving money on the table. We’re doubling down on affiliate ecosystems, performance-driven creator partnerships, and cross-platform analytics to ensure our brands win where consumers are already shopping.

5. Retail Strategy Is No Longer Binary. It’s a Dynamic Mix

In the past, a brand typically had to choose:

→ Go DTC and own the customer

→ Or go retail for reach and validation

Today, that’s no longer the case. The most successful beauty brands are executing multi-platform strategies that blend DTC, traditional retail, and emerging marketplaces and tailoring their presence by channel, audience, and category. The consumer is now everything, everywhere, all at once. Demand is coming from every direction, and brands are increasingly agnostic about where the conversion happens. What matters most is getting the consumer into your funnel. Where does your consumer want to shop? Listen to that and meet them there.

For TBV brands, this dynamic presents an opportunity — and a challenge. We help founders:

Decide when to go retail and who those partners should be

Evaluate the long-term value of exclusivity vs. scale (not mutually exclusive)

Launch with platform fluency, from TikTok to Amazon to Sephora

Looking Ahead: What Does Retail Readiness Really Mean?

In 2025, “retail readiness” isn’t just about having the right packaging / shelf presence or nailing your retailer meetings.

It’s about:

Owning your creator economy funnel

Understanding which channel drives your best customers

Having a platform strategy, not just a retail one

As we enter this next chapter of the beauty retail evolution, our job is to help early-stage founders enter and navigate this new world. One where discovery is social, conversion is instant, and brand equity is built across platforms, not just shelves.

https://www.glossy.co/beauty/tiktokmademebuyit-is-driving-amazon-beauty-sales/

Jefferies Equity Research Report Insight: Deep Dive Into the Beauty Retail Market; Concern for Ulta as Ecom Wins March 2025

Jefferies Equity Research Report Insight: Deep Dive Into the Beauty Retail Market; Concern for Ulta as Ecom Wins March 2025

Thanks for the great insights, Cristina! With TikTok and Amazon leading the charge online, the Sephora/Ulta duopoly is definitely under attack. At least they still hold an edge with in-store discovery.

But even there, I feel older millennials and Gen X might have “graduated” from Sephora and Ulta and are seeking a more elevated experience. Curious to know who you think might be best positioned to capture these customers?

This is exactly what I want to read. Subscribed!